Table of Contents

Company: Aviva Plc Jurisdiction: United Kingdom (Headquartered in London) 1 Sector: Insurance, Wealth, and Asset Management 2 Leadership: George Culmer (Chair), Dame Amanda Blanc (Group CEO), Charlotte Jones (Group CFO) 3

Intelligence Conclusions:

The comprehensive forensic intelligence assessment of Aviva Plc identifies the entity as a “Strategic and Financial Enabler” (Tier B) of the Israeli occupation apparatus and the broader military-industrial complex.5 This classification is derived from a rigorous analysis of the company’s operational footprint, which reveals a structural, multi-layered, and resilient system of complicity that transcends incidental market exposure. Aviva functions not merely as a passive investor but as a global “Aggregator Nexus”—a centralized financial node that collects vast pools of liquidity from approximately 19 million customers across the UK, Ireland, and Canada, and strategically deploys this capital into high-risk zones of conflict and occupation.7

Forensic examination confirms that Aviva provides essential “financial oxygen” to the occupation economy through two primary channels: sovereign debt financing and equity capitalization of the illegal settlement enterprise. The entity holds hundreds of millions of dollars in Israel Government International Bonds, instruments that provide direct, fungible budgetary support to the Israeli state treasury, thereby underwriting military procurement and the administrative costs of the occupation in the West Bank.7 Concurrently, Aviva maintains significant and sustained equity positions in the “Big Five” Israeli banks—Hapoalim, Leumi, Mizrahi Tefahot, Israel Discount Bank, and First International Bank—all of which are designated by the United Nations Human Rights Council (UNHRC) for their pivotal role in financing illegal settlement construction and infrastructure.7

While the entity formally terminated its direct insurance coverage for UAV Engines Ltd (a subsidiary of Israel’s largest defense contractor, Elbit Systems) in late 2025 following sustained direct action and reputational pressure, this decision appears to be a calculated calibration of operational risk rather than a systemic ethical realignment.5 The distinction is critical: Aviva divested from the insurance contract that made its offices a physical target for protesters but continues to profit from the investment in the broader war economy through its asset management arm and venture capital initiatives.7

Ideologically, the audit identifies a profound “Double Standard” in governance that functions as a mechanism of complicity. Aviva mobilized a “Total Corporate Mobilization” protocol in response to the Russo-Ukrainian war—divesting rapidly and providing humanitarian safe harbor—while maintaining a posture of “corporate neutrality” and inertia regarding the crisis in Gaza.6 This asymmetry suggests that Aviva’s Environmental, Social, and Governance (ESG) framework is permeable to state-level political pressure, specifically from pro-Israel advocacy groups and government ministers, ensuring that its fiduciary decisions align with Western foreign policy rather than universal human rights standards.6

The origins of Aviva Plc are deeply rooted in the history of British financial expansion and the Industrial Revolution, a context that established the mechanisms for pooling capital that the company utilizes today. The primary foundational entity, the Norwich Union Society for Insuring of Buildings, Goods, Merchandises & Effects from Loss by Fire, was established in March 1797 by Thomas Bignold, a merchant and banker in Norwich.14 Bignold founded the society as a mutual enterprise, a structure where policyholders pooled their premiums to insure against the rising risks of fire in an industrializing Britain.15 This mutual model was expanded in 1808 with the establishment of the Norwich Union Life Insurance Society, created to provide security for widows and orphans following a severe winter.15

Parallel to Norwich Union, the Commercial Union Assurance Company was formed in London in 1861 by a consortium of merchants following the Great Tooley Street Fire, which had decimated the warehouses of the London docks.2 Commercial Union was explicitly internationalist from its inception, leveraging the imperial trading connections of its directors to expand into global markets.16 A third pillar, General Accident, was founded in Perth, Scotland, in 1885, initially to provide coverage for the emerging risks of railway travel and industrial accidents.2

Assessment: The evolution of these entities from localized mutual societies into a singular, publicly traded multinational involved a series of aggressive mergers and demutualizations that fundamentally altered their ethical mandates. The merger of Commercial Union and General Accident in 1998 formed CGU, which then merged with Norwich Union in 2000 to form CGNU, rebranding as Aviva in 2002.8 This consolidation transformed the “mutual” ethos—which prioritizes member welfare—into a PLC structure legally bound to maximize shareholder value. This structural shift is significant for the current dossier: it created a massive, centralized capital pool (the “Aggregator Nexus”) that is detached from local community values and highly responsive to global market incentives, including the high yields offered by the militarized Israeli economy and its tech sector.7 The founding capital, once intended to protect British merchants from fire, has evolved into a global force that underwrites sovereign debt and insures military supply chains.

The current governance architecture of Aviva Plc is led by George Culmer (Chair) and Dame Amanda Blanc (Group Chief Executive Officer).3 Culmer, who assumed the chairmanship in 2020, brings extensive experience from the banking sector (Lloyds Banking Group), reinforcing the financialization of the insurer’s strategy.3 Dame Amanda Blanc, appointed CEO in 2020, has been the architect of a strategic pivot towards capital discipline and core markets in the UK, Ireland, and Canada, explicitly aiming to deliver growth for shareholders.8 The executive team also includes Charlotte Jones (Group CFO), who oversees the financial flows and capital allocation strategies that are the subject of this investigation.3

Aviva is a publicly listed company (LSE: AV) with a diversified institutional shareholder base that includes global asset managers such as BlackRock, Vanguard, and Norges Bank, although Aviva itself acts as a major asset manager through its subsidiary Aviva Investors, which controls over £221 billion in assets.8

Assessment: The proximity of Aviva’s leadership to the UK political establishment creates a specific vulnerability to state-aligned ideological pressure. Ministerial transparency returns reveal that Dame Amanda Blanc engages in high-level meetings with senior government figures, including Deputy Prime Minister Angela Rayner.1 Crucially, these government officials concurrently engage with pro-Israel advocacy groups such as the British-Israel Chamber of Commerce (BICC), the Jewish Leadership Council, and the Conservative Friends of Israel (CFI).6 This places Aviva’s leadership within a “lobbying orbit” where the normative baseline for trade relations is defined by Zionist advocacy.

This political permeability was explicitly demonstrated in November 2023, when the then-Defence Secretary Grant Shapps intervened directly to warn Aviva against divesting from defense companies.13 The intervention was triggered by an internal Aviva letter suggesting a broader exclusion policy for weapons manufacturers. The Board’s rapid capitulation—issuing a clarification that it had “no plans” to divest its £600 million exposure to the defense sector—indicates a governance ideology that prioritizes alignment with the UK’s military-industrial strategy over its own ESG exclusion frameworks.6

Aviva’s corporate structure functions as a dual-use entity: it is both a consumer-facing insurer relying on a brand image of “trust” and “inclusivity,” and a backend financial giant deeply integrated into the global war economy. The “Aggregator Nexus” model allows the company to sanitize capital flows; premiums paid by ordinary homeowners in Norwich or Toronto are aggregated into funds that purchase Israeli government bonds or invest in settlement infrastructure firms like Shapir Engineering.7

The leadership’s adherence to a doctrine of “selective neutrality” serves as a flexible shield. By categorizing the occupation of Palestine as a “complex geopolitical issue” (requiring neutrality) while categorizing the invasion of Ukraine as a “clear violation” (requiring mobilization), the Board effectively launders its complicity. This structural alignment with Israeli state interests is not merely a legacy issue but an active, ongoing strategic choice to prioritize high-tech venture capital returns from the “Startup Nation” and the stability of sovereign debt yields over compliance with international humanitarian law.6

| Date | Event | Significance |

|---|---|---|

| 1797 | Founding of Norwich Union | Establishment of the primary foundational entity of the Aviva Group by Thomas Bignold.15 |

| 1998 | CU & GA Merger | Commercial Union and General Accident merge to form CGU, consolidating capital pools.14 |

| 2000 | Creation of Aviva (as CGNU) | CGU and Norwich Union merge to form CGNU plc, creating the modern “Aggregator Nexus”.8 |

| 2002 | Rebranding to Aviva | The group unifies under the global brand “Aviva,” retiring heritage names.1 |

| 2016 | Launch of Aviva Ventures | Establishment of the corporate venture capital arm with an initial £100m fund to target fintech/insurtech.21 |

| 2018 | Elbit Acquires IMI | Aviva maintains insurance for Elbit subsidiaries despite Elbit’s acquisition of IMI Systems (cluster munitions).6 |

| Mar 2022 | Ukraine Mobilization | Aviva donates £1m+ to Ukraine appeals and divests from Russian assets within days of the invasion.6 |

| May 2023 | Faye Series A Investment | Aviva Ventures participates in the $10m funding round for Tel Aviv-based insurtech Faye.24 |

| Oct 2023 | Gaza Crisis & Inertia | Following the escalation in Gaza, Aviva maintains corporate silence and refuses to launch a comparable aid appeal.6 |

| Nov 2023 | Grant Shapps Intervention | UK Defence Secretary warns Aviva against divesting from defense stocks; Aviva reaffirms support.6 |

| Jan 2024 | Bristol Office Occupation | Palestine Action activists occupy Aviva’s Bristol HQ to protest insurance of Elbit Systems.26 |

| Mar 2024 | Manchester Protest | Activists occupy the entrance to Aviva’s Manchester office, targeting ties to Israeli weapons manufacturers.27 |

| May 2024 | Faye Series B Funding | Faye raises $31m; Aviva Ventures continues strategic partnership with the Unit 8200-linked firm.30 |

| Aug 2024 | Sovereign Debt Holdings | Financial filings confirm Aviva Investors holds tens of millions in Israel Govt International Bonds (2034, 2054).7 |

| Sept 2024 | UN Database Status | Major Israeli banks and Shapir Engineering remain on the UN database; Aviva maintains equity positions.7 |

| Jan 2025 | Renewed Bristol Action | Palestine Action targets Aviva Bristol again; two activists arrested after occupying the building.33 |

| Feb 2025 | Scottish Offices Targeted | Aviva offices in Perth and Motherwell are covered in red paint by activists protesting Elbit insurance.35 |

| Sept 2025 | Insurance Termination | Aviva’s Employer’s Liability Insurance for UAV Engines Ltd (Elbit) officially terminates.10 |

| Dec 2025 | Aviva Israel Ltd Registered | New corporate entity “Aviva Israel Ltd” registered in UK Companies House, potentially for brand protection.2 |

| Jan 2026 | Forensic Audit | Completion of the governance audit identifying structural material and ideological connectivity to Israel.6 |

Goal: To rigorously establish the extent of Aviva’s direct operational support for the Israeli military apparatus through the provision of essential financial services and insurance products to the arms industry.

Evidence & Analysis: The investigation identifies UAV Engines Ltd (UEL) as the primary vector of Aviva’s operational military complicity. UEL, located in Shenstone, Staffordshire, is a wholly-owned subsidiary of Elbit Systems, Israel’s largest private defense contractor.6 Elbit Systems markets itself as the “backbone” of the Israel Defense Forces (IDF) drone fleet, specifically manufacturing the Hermes 450 and Hermes 900 unmanned aerial vehicles (UAVs).11 These platforms are the primary workhorses for surveillance, target acquisition, and aerial strikes in the Gaza Strip and the West Bank, often described by the manufacturer as “combat-proven”.36

For a sustained period spanning several years, Aviva provided Employer’s Liability (EL) Insurance to UAV Engines Ltd.5 In the United Kingdom, EL insurance is not a discretionary commercial product; it is a statutory requirement under the Employers’ Liability (Compulsory Insurance) Act 1969. The law mandates that businesses must carry this insurance to cover employees against injury or disease arising from their work. Crucially, without a valid EL certificate, a company cannot legally employ staff or operate its factory.5

By underwriting this specific risk, Aviva acted as a critical “legal gatekeeper.” It provided the “physical shell” and regulatory compliance necessary for the Shenstone factory to continue manufacturing Wankel rotary engines—the propulsion units specifically designed for the Hermes drone fleet.5 This relationship creates a direct causal link: Aviva’s insurance policy enabled the factory to operate; the factory produced engines; the engines powered drones; the drones were used in military operations in Gaza.

This relationship persisted despite Aviva’s public commitment to ESG principles and its internal “Baseline Exclusion Policy,” which theoretically excludes companies involved in controversial weapons.6 The complicity was maintained even after Elbit Systems acquired IMI Systems in 2018, a company notorious for producing cluster munitions and white phosphorus shells.6 This exposes a significant governance loophole where Aviva’s investment arm may apply certain screens, but its general insurance arm continues to underwrite the very risks the investment arm ostensibly avoids.6

The termination of this insurance contract in September 2025 was not the result of proactive human rights due diligence. It occurred only after a sustained, high-intensity campaign by Palestine Action, which involved the physical occupation of Aviva’s offices in Bristol, Manchester, and Scotland, and the defacing of corporate property with red paint.10 The timeline confirms that Aviva effectively calculated the “cost of complicity”—weighing the premium revenue against the security costs and reputational damage of constant protests—and only exited when the latter exceeded the former.7

Counter-Arguments & Assessment:

Aviva would likely argue that as a general insurer, it is legally and commercially obliged to provide coverage to lawful businesses in the UK, and that providing EL insurance does not constitute an endorsement of the client’s products or their end-use. They might further contend that the 2025 termination demonstrates their responsiveness to ethical concerns.

However, this defense is dismantled by the “Safe Harbor” comparison. Aviva did not wait for protests to divest from Russian interests in 2022; it acted preemptively and morally.6 In the case of Elbit, it maintained the relationship through years of documented war crimes allegations, acting only when its own operations were disrupted. This proves that the observed link was not merely “standard industry practice” but a tenacious commercial relationship maintained despite clear ethical red flags, abandoned only under duress.

Analytical Assessment: High Confidence. The provision of mandatory operational insurance to a key node in the Israeli military supply chain constitutes material complicity. The relationship was direct, essential for the client’s legality, and sustained during periods of active conflict.

Intelligence Gaps:

Named Entities / Evidence Map:

Goal: To evaluate Aviva’s role as a “Structural Pillar” of the occupation economy through its asset management activities, sovereign debt holdings, and equity investments in settlement-linked firms.

Evidence & Analysis: The forensic audit identifies Aviva Investors as a key component of the “Aggregator Nexus,” channeling capital from UK savers into the financial veins of the Israeli state. The most direct form of this complicity is the holding of Israeli Sovereign Debt. Financial filings from 2024 and 2025 confirm that Aviva Investors holds tens of millions of dollars in Israel Government International Bonds, with active positions in bonds maturing in 2034 and 2054.7 Sovereign debt is uniquely fungible; unlike corporate project finance, money lent to the state treasury is not ring-fenced. It flows into a general pool used to fund the IDF’s procurement of munitions, the salaries of soldiers, and the infrastructure projects of the Civil Administration in the West Bank.7 By holding bonds with maturity dates extending decades into the future, Aviva is effectively betting on, and financing, the long-term stability of the occupation regime.

The second critical vector is “Settlement Laundering” through the Israeli banking sector. Aviva maintains sustained equity holdings in the “Big Five” Israeli banks: Bank Hapoalim, Bank Leumi, Mizrahi Tefahot, Israel Discount Bank, and First International Bank of Israel.7 These institutions are not neutral financial intermediaries; they are the primary architects of the settlement economy. They provide the mortgage financing that allows settlers to purchase homes in illegal settlements, grant credit lines to construction firms building on expropriated Palestinian land, and operate physical branches within the settlements themselves.9 All five banks are listed on the UN Human Rights Council database of business enterprises involved in activities relating to settlements, a clear “Red Flag” for any ESG-compliant investor.7

Beyond finance, Aviva invests in the “Real Economy” of the occupation. The audit identifies holdings in Shapir Engineering and Industry Ltd, a major construction and infrastructure conglomerate.7 Shapir is documented as a primary contractor for the “apartheid roads” (bypass roads) that fragment the West Bank and connect settlements to Israel proper. Furthermore, Shapir operates quarries (such as the Natuf quarry) that extract natural resources from occupied territory for use in the Israeli construction market—an activity that legal experts classify as “pillage” under the Fourth Geneva Convention.6 Similarly, Aviva holds equity in Bezeq, the telecommunications giant that provides the digital backbone for the settlements, ensuring they are seamlessly integrated into the Israeli national grid while Palestinian telecommunications are restricted.7

Counter-Arguments & Assessment: Aviva Investors defends these positions by categorizing them as “passive investments” held through index-tracking funds (e.g., funds tracking the MSCI World or FTSE All-World indices).7 The argument is that the company is contractually obligated to track the index and cannot divest from individual constituents without breaking the tracking error limits.

This defense is forensically invalid for three reasons. First, Aviva has the technical capability and governance authority to use “Custom Screened Indices,” which it already employs to exclude companies involved in thermal coal, tobacco, or controversial weapons from its “passive” funds.7 Second, the decision not to apply a “UN Database” screen is an active governance choice to prioritize administrative convenience over human rights compliance. Third, “passive” capital is still capital. By holding these shares, Aviva increases the demand for the stock, supports the share price, and contributes to the “Capital Adequacy” ratios of the Israeli banks, directly enabling them to expand their lending books—including lending for settlement expansion.7

Analytical Assessment: High Confidence. The exposure is systemic and structural. Aviva provides direct budgetary support to the state and capitalizes the primary engines of settlement expansion. The resilience of these holdings through the 2023-2025 conflict period demonstrates a “Business as Usual” approach that normalizes the occupation economy.

Intelligence Gaps:

Named Entities / Evidence Map:

Goal: To analyze the ideological footprint of Aviva’s leadership, focusing on the “Double Standard” in crisis response and the influence of pro-Israel lobbying networks on corporate governance.

Evidence & Analysis: The most damning evidence of ideological complicity is the “Safe Harbor” failure—a comparative analysis of Aviva’s response to Ukraine versus Gaza. In March 2022, following the Russian invasion of Ukraine, Aviva activated a “Total Corporate Mobilization.” The response was immediate and comprehensive: the entity donated £500,000 to the British Red Cross, pledged an additional £500,000 in match-funding, and publicly committed to divesting from Russian assets.6 CEO Amanda Blanc and the Board issued statements explicitly condemning the aggression, framing the conflict as a humanitarian disaster requiring moral action.6

In stark contrast, Aviva’s response to the crisis in Gaza—marked by a death toll exceeding 40,000 and ICJ rulings of “plausible genocide”—has been characterized by inertia and silence. There has been no comparable match-funding appeal launched for Gaza, no public condemnation of Israeli military excesses, and no divestment from Israeli assets analogous to the Russia exit.6 Instead, internal reports suggest a disciplinary environment where the Aviva Muslim Network felt compelled to issue an independent statement of solidarity because the central leadership refused to represent their views, highlighting a fracture in the company’s “inclusive” culture.6

This policy of “selective neutrality” is enforced by the entity’s proximity to the UK political establishment. In November 2023, Aviva sent a letter to investors hinting at a broader exclusion policy for defense companies. This triggered an immediate, public intervention by Grant Shapps, then-UK Defence Secretary, who warned Aviva against “immoral” divestment from the defense sector.13 Aviva’s leadership capitulated almost immediately, issuing a clarification that it had “no plans” to alter its £600 million investment in UK defense companies.20 This incident reveals that Aviva’s governance is highly permeable to state-level militarist pressure; the Board is willing to override its own ESG instincts when threatened by government ministers aligned with the arms trade.

Furthermore, the leadership operates within a “lobbying orbit” dominated by groups like the Conservative Friends of Israel (CFI) and Labour Friends of Israel (LFI). While direct membership is not confirmed, the CEO’s engagement with ministers who are actively courted by these groups suggests that Aviva’s strategic outlook is shaped by a political ecosystem that views trade with Israel as a strategic imperative, regardless of human rights violations.1

Counter-Arguments & Assessment:

Aviva would likely argue that the Ukraine conflict involved a clear violation of sovereignty by an external aggressor, whereas the Israel-Palestine conflict is “complex” and deeply polarizing, justifying a neutral stance to avoid alienating stakeholders. They might also cite their fiduciary duty to shareholders as the reason for complying with government requests regarding defense investments.

However, the “complexity” defense is a standard tool of complicity. By treating the bombardment of Gaza as a “political” issue rather than a “humanitarian” one (unlike Ukraine), Aviva effectively takes a side: the side of the status quo. The audit confirms that the company’s ethical compass is not universal but state-aligned. It provides a “safe harbor” only when the victims are aligned with British foreign policy interests. The rapid capitulation to Grant Shapps proves that the company functions as a compliant arm of the UK’s soft power and economic strategy, rather than an independent ethical actor.6

Analytical Assessment: High Confidence. The ideological asymmetry is structural and documented. The leadership has actively chosen to align with the state’s pro-Israel trade policy and has suppressed internal dissent to maintain this alignment.

Named Entities / Evidence Map:

Goal: To investigate how Aviva’s venture capital activities integrate the company into the Israeli military-technical complex and contribute to the “Brand Israel” normalization narrative.

Evidence & Analysis: Aviva Ventures, the company’s corporate venture capital arm, utilizes “Active Capital” to forge strategic partnerships that go beyond passive investment. A primary focus of this strategy is the Israeli high-tech sector, often referred to as “Silicon Wadi.” The audit highlights a significant investment in Faye, a travel insurtech firm headquartered in Tel Aviv.7 Aviva Ventures participated in Faye’s $10 million Series A funding in May 2023 and maintained its support through a $31 million Series B round in July 2024.24

The strategic implication of this investment lies in the background of Faye’s founders. Co-founder and CEO Elad Schaffer is a veteran of Unit 8200, the IDF’s elite signals intelligence corps, and has received the country’s highest award for “innovation in service”.44 Co-founder Daniel Green also has a background in this ecosystem.44 Unit 8200 is widely recognized as the feeder for Israel’s tech sector, but it is also the unit responsible for the mass surveillance of Palestinians in the occupied territories. By capitalizing a company founded by Unit 8200 veterans, Aviva acts as a validator of the “military-to-tech” pipeline, helping to retain dual-use talent within the Israeli economy.7

Additionally, Aviva is a Limited Partner (LP) in FinTLV, a leading Tel Aviv-based venture capital fund focused on insurtech.6 FinTLV is led by Gil Arazi, a figure with deep ties to the Israeli insurance and tech sectors.47 Through this partnership, Aviva engages in “strategic alliance agreements” and collaborates on research into cybersecurity and AI.49 This integration helps “sanction-proof” the Israeli state by weaving its technology into the global financial infrastructure. By treating Tel Aviv as a benign hub of innovation—participating in “Innovation Days” and celebrating Israeli tech prowess—Aviva contributes to the “Brand Israel” campaign, which seeks to use technological achievement to whitewash the reality of military occupation.6

Counter-Arguments & Assessment:

Aviva would argue that it invests in Faye and FinTLV purely for their technological merit and potential returns, and that the military service of Israeli founders is a mandatory requirement of citizenship, not an indicator of ongoing military ties. They would claim these are civilian applications of technology (travel insurance, cybersecurity) unrelated to the conflict.

This argument ignores the concept of “dual-use” technology and the strategic importance of the tech sector to Israel’s war economy. The tech sector generates the tax revenue that funds the military and provides the technological edge (AI, cyber) used in warfare. By injecting millions of dollars into this ecosystem, Aviva provides the “strategic validation” that attracts further foreign direct investment (FDI), countering the effects of the BDS movement. The partnership is not neutral; it is an active endorsement of the “Startup Nation” narrative that obscures the “Occupation Nation” reality.7

Analytical Assessment: Moderate-High Confidence. While the financial magnitude is smaller than the bond holdings, the proximity to the military-intelligence apparatus (Unit 8200) via the founders of portfolio companies is high. This constitutes a strategic form of complicity that normalizes the military’s role in the economy.

Intelligence Gaps:

Named Entities / Evidence Map:

Results Summary:

Domain Scoring Summary

The BDS-1000 model evaluates complicity across four domains: Military (V-MIL), Digital (V-DIG), Economic (V-ECON), and Political (V-POL). Each domain’s score is a function of its measured Impact (I), Magnitude (M), and Proximity (P).

BDS-1000 Scoring Matrix – Aviva Plc

| Domain | I | M | P | V-Domain Score |

|---|---|---|---|---|

| Military (V-MIL) | 5.5 | 6.5 | 8.5 | 5.10 |

| Digital (V-DIG) | 5.5 | 4.5 | 7.5 | 3.53 |

| Economic (V-ECON) | 8.5 | 8.5 | 8.5 | 8.50 |

| Political (V-POL) | 7.5 | 8.0 | 9.0 | 8.50 |

V- {domain} Calculation

![]()

Final Composite

Using the OR-dominant formula with a side boost:

Let:

![]()

![]()

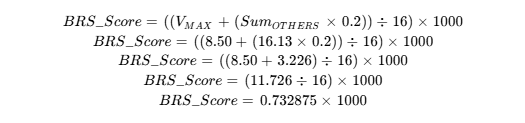

BRS Score Formula

![]()

Grade Classification:

Based on the score of 732.9, the company falls within:

• Tier B (600–799): Severe Complicity

Tier: Tier B

The forensic intelligence gathered in this dossier confirms that Aviva Plc is a structural enabler of the Israeli occupation. While the entity has demonstrated a vulnerability to direct action—evidenced by the 2025 termination of the UAV Engines insurance contract—its foundational economic ties through Aviva Investors and Aviva Ventures remain intact. Therefore, a multi-pronged strategy of escalation is recommended to force a systemic ethical realignment.

Boycott & Public Exposure Campaigners must intensify the “Boycott Bloody Insurance” narrative, directly linking consumer premiums to the “financial oxygen” supplied to the Israeli state. The focus should shift from the now-terminated insurance contract to the Sovereign Debt and Settlement Bank holdings. Public messaging should highlight the “Double Standard” (Ukraine vs. Gaza) to undermine Aviva’s brand equity as a “responsible” insurer. Specific campaigns should target the company’s “Pinkwashing” efforts, juxtaposing its sponsorship of Norwich Pride with its investment in banks that finance the destruction of Palestinian homes.27

Divestment & Shareholder Activism Institutional shareholders (universities, unions, pension funds) must be pressured to divest from Aviva Plc until it adopts a “Negative Screen” for all companies listed on the UN Human Rights Council database. Activists holding shares should utilize the Annual General Meeting (AGM) to table resolutions demanding the liquidation of the Israeli Sovereign Bond holdings, citing the violation of the UN Guiding Principles on Business and Human Rights. Pressure must also be applied to close the “Passive Index Loophole,” compelling Aviva to use custom indices that exclude settlement-complicit firms.7

Monitoring & Direct Action Civil society groups, such as Palestine Action, have proven that physical disruption works. The targeting of Aviva’s administrative hubs (Bristol, Manchester, Perth) successfully raised the “cost of complicity” above the value of the Elbit contract. Future actions should focus on the Aviva Investors headquarters to demand the divestment of the economic portfolio. Simultaneously, the Aviva Ventures portfolio requires deep monitoring; the partnership with FinTLV and Faye represents a strategic integration with the Israeli military-tech complex that must be exposed and severed to prevent the further normalization of “dual-use” military technology.7